Chapter 5: RCM Under Section 9(4) — Purchases from Unregistered Suppliers

This is where many businesses get confused — and where things used to be extremely complicated.

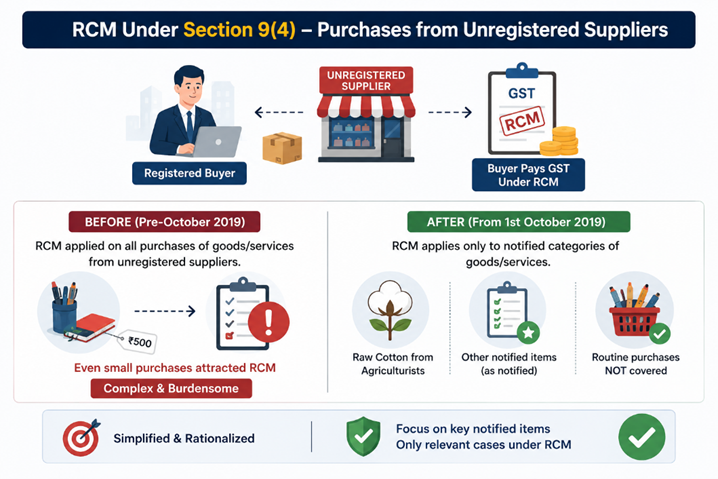

The Original Rule (Pre-October 2019)

Under Section 9(4), if a registered person bought any goods or services from an unregistered supplier, RCM applied.

This was a nightmare for businesses — imagine a registered company buying stationery worth ₹500 from a local shop, having to self-invoice and pay GST on it!

The government suspended this provision multiple times and finally brought in a completely revised version effective October 1, 2019.

The Current Rule

RCM under Section 9(4) now applies only to specific notified categories of goods/services purchased from unregistered suppliers by registered persons.

Currently, the following have been notified:

- Raw Cotton purchased from agriculturists (as above)

- Other items as specifically notified from time to time

For most routine purchases from unregistered vendors (stationery, small repairs, miscellaneous), Section 9(4) RCM does not apply for now.

Chapter 6: Who Must Comply?

If You Are a Recipient Liable Under RCM:

Step 1: Self-Invoice You must issue a self-invoice (since the supplier won't issue a proper GST invoice). This documents the transaction for your records.

Step 2: Pay GST in Cash Unlike normal ITC credits, you cannot use your ITC balance to pay RCM liability. RCM GST must be paid in cash (through your electronic cash ledger).

Step 3: Claim ITC Here's the silver lining — after paying RCM in cash, you can claim that same amount back as Input Tax Credit (ITC), provided the goods/services are used for business purposes.

So the net cash flow impact is often zero for fully eligible businesses.

Step 4: Report in GSTR-3B RCM liability must be declared in Table 3.1(d) of GSTR-3B (Outward supplies under RCM — wait, it's actually inward supplies attracting reverse charge). ITC claimed is reported in Table 4(A)(3).

Chapter 7: Where RCM Does NOT Apply

Let's clear up some common misconceptions.

❌ Purchases from Registered Suppliers (Generally)

If you buy from a GST-registered vendor who charges GST on their invoice, this is normal forward charge. RCM doesn't apply. The supplier collects and deposits the tax.

❌ Small Purchases from Unregistered Vendors (Under Current Rules)

After the 2019 amendment, routine purchases from your neighbourhood grocery or hardware store don't trigger RCM for most businesses. (Subject to specific notifications.)

❌ Services Received by Non-Business Individuals

Ramesh's personal legal advice from an advocate? No RCM. RCM on legal services applies only when the recipient is a business entity.

❌ GTA Services Where GTA Has Opted for Forward Charge

If the GTA has declared and opted to pay GST under forward charge, the recipient is relieved of RCM liability.

❌ Composition Dealers as Recipients

Wait — here's a twist! If you are a Composition Scheme dealer, you still have RCM liability on notified supplies. But you cannot claim ITC on what you pay under RCM. This makes RCM a genuine cost for composition dealers.

❌ Exempt Goods/Services

If the goods or services themselves are exempt from GST, RCM doesn't apply even if the supplier is unregistered. No GST = no RCM.

Chapter 8: The Composition Dealer Trap

Meet Suresh, a small restaurant owner registered under the GST Composition Scheme. He pays 5% composition tax on his turnover and enjoys simplified compliance.

One day, he hires a local transporter (GTA) to deliver supplies. Under RCM, Suresh must pay GST on the freight charges. He pays ₹2,000 as GST under RCM.

But — he cannot claim ITC, because composition dealers are barred from claiming input tax credit.

So that ₹2,000 is a real cost to Suresh. No offset. No relief.

This is the composition dealer trap — RCM liability without the ITC benefit. Suresh must factor this into his pricing.

Chapter 9: Registration Requirement Under RCM

Here's an interesting rule many people miss:

A person who is exclusively liable to pay tax under RCM must mandatorily register for GST, even if their turnover is below the threshold limit.

Example: A small NGO in Delhi receives services from a foreign entity (import of services). Even if the NGO's turnover is below ₹20 lakh, it must register for GST solely to comply with RCM obligations.

Conclusion

The Reverse Charge Mechanism (RCM) is an important provision under GST that shifts the responsibility of tax payment from the supplier to the recipient in specified cases. Through Sections 9(3) and 9(4), the government aims to ensure better tax compliance, bring unorganized sectors into the tax net, and prevent revenue leakage.

While RCM strengthens the GST framework, it also places additional compliance responsibilities on businesses, such as identifying applicable transactions, timely payment of tax, proper accounting, and accurate reporting in GST returns. Failure to comply may lead to interest, penalties, and denial of input tax credit.

Therefore, businesses must regularly review their transactions, stay updated with changes in GST provisions, and maintain proper documentation to ensure smooth compliance. A clear understanding of RCM not only helps avoid legal consequences but also enables businesses to manage their tax obligations efficiently and confidently.